Authored by the expert who managed and guided the team behind the Sweden Property Pack

Everything you need to know before buying real estate is included in our Sweden Property Pack

Sweden is one of the few European countries where foreigners, including Americans, can buy residential property with virtually no legal restrictions, which makes it a surprisingly open market for US buyers looking at Scandinavia.

In this guide, we break down everything from stamp duty and mortgage rules to FATCA reporting and neighborhood tips, all based on official Swedish sources and updated to reflect the latest 2026 figures.

We constantly update this blog post so that every number and rule you read here stays current and reliable.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Sweden.

Can a US citizen legally buy residential property in Sweden right now?

Can I buy a home in Sweden as a US citizen in 2026?

As of early 2026, US citizens can legally purchase any type of residential property in Sweden, whether it is a house, an apartment building, or a cooperative apartment (called a bostadsratt), because Sweden has no nationwide restriction preventing foreigners from buying homes.

The standard process for a US citizen buying a home in Sweden follows the same steps as a local buyer: you find a property (often through a Swedish real estate agent), place a bid, sign a purchase contract (kopekontrakt), and then register ownership with Lantmateriet, which is Sweden's official land registration authority.

What makes Sweden stand out is that your American passport does not add any extra legal hurdle to the purchase itself, so the real friction points are usually practical ones like getting a Swedish bank account, securing financing, and handling the paperwork in Swedish.

By the way, we've written a blog article detailing all the foreigner rights regarding properties in Sweden.

Are there many Americans buying property and living in Sweden in 2026?

As of early 2026, there are roughly 25,000 US-born residents registered in Sweden according to Statistics Sweden (SCB), and community estimates that include dual citizens suggest the broader American community in Sweden could be closer to 40,000 to 50,000 people.

Most American expats in Sweden cluster in Stockholm's popular neighborhoods like Sodermalm, Ostermalm, and Kungsholmen, as well as in Gothenburg's Majorna and Centrum districts and in Malmo's Vastra Hamnen area, largely because these areas have strong international school access and English-friendly services.

The top three reasons Americans choose to buy property and relocate to Sweden are the country's strong work-life balance and generous parental benefits, job opportunities in Sweden's thriving tech sector (think Spotify, Ericsson, and Klarna), and access to high-quality public healthcare and education.

The American expat community in Sweden has been gradually growing over the past few years, driven by rising interest in Nordic quality of life and an increase in remote work arrangements that let US professionals live abroad while keeping their American income.

Do foreigners have the same buying rights as locals in Sweden?

In Sweden, foreign buyers, including Americans, have essentially the same legal right to purchase residential property as Swedish citizens, and there is no special surcharge, extra tax, or additional permit required because of your nationality.

No property type or location in Sweden is formally off-limits to foreign buyers, but the one area where things get slightly more nuanced is cooperative apartments (bostadsratt), because the housing cooperative's board must approve you as a member, and some boards may be more cautious with non-resident applicants or buyers without a clear connection to Sweden.

We cover all these things in length in our pack about the property market in Sweden.

Can I buy property in Sweden without a residence permit?

You do not need a Swedish residence permit to buy property in Sweden, so Americans living in the US or anywhere else in the world can legally purchase a home here without any immigration requirement.

The process for buying property in Sweden while living abroad is essentially the same as for a local buyer: you can sign contracts, transfer funds, and register ownership remotely, though many non-residents choose to use a Swedish lawyer or a power of attorney to handle paperwork on the ground.

Buying a home in Sweden does not grant you any visa or residency rights, so if you want to actually live in Sweden long-term, you will still need to apply for a residence permit through the Swedish Migration Agency separately.

The main practical challenge non-resident buyers face when completing a purchase remotely in Sweden is securing a mortgage, because most Swedish banks prefer borrowers with a Swedish personal identity number and documented Swedish income, which makes financing significantly harder from abroad.

Can US citizens own land in Sweden?

Yes, US citizens can own land outright in Sweden, because Swedish law allows foreign individuals to register full freehold ownership (called aganderatt) of real property, including the land underneath a house.

In Sweden, the main distinction is between aganderatt, where you own both the building and the land, and tomtratt, a long-term municipal leasehold where you own the building but lease the land from the local government, and both options are available to foreign buyers without restriction.

There are no geographic zones or land categories in Sweden where foreign ownership is specifically restricted or prohibited, which sets Sweden apart from several other European countries that limit agricultural or coastal land sales to non-residents.

Getting surprised by hidden fees is one of the pitfalls people face when buying real estate in Sweden.

What documents will I need to buy in Sweden?

To purchase residential property in Sweden as a US citizen, you will typically need your passport, a signed purchase contract (kopekontrakt), proof of funds or source of funds documentation for anti-money laundering checks, and, if you are financing the purchase, income statements and bank records.

A Swedish tax identification number is not strictly required to complete the purchase itself, but if you earn rental income or have other Swedish tax obligations, Skatteverket can issue you a special coordination number (samordningsnummer) or tax registration number that you apply for directly through the Swedish Tax Agency.

A local Swedish bank account is not legally mandatory to buy property in Sweden, but in practice almost every buyer opens one because it makes paying the deposit, closing costs, and ongoing bills (like cooperative fees or property charges) much simpler and faster.

Swedish banks and real estate agents will almost always ask you for proof of funds showing where your money comes from, and while a Swedish address is not strictly required for the purchase, having one helps significantly with banking applications and mail delivery for important documents.

We have a whole section dedicated to all the documents you need in our Sweden property pack.

Can a foreign-owned company buy property in Sweden?

Yes, a foreign-owned company can legally purchase residential property in Sweden, and there is no restriction preventing a US-owned entity from registering ownership of a Swedish home.

Americans who want to use a corporate structure to hold property in Sweden typically set up a Swedish aktiebolag (AB), which is the local equivalent of a limited company, because Swedish banks and authorities strongly prefer dealing with a Swedish-registered entity rather than a US LLC.

Owning property through a company in Sweden does not automatically lower your taxes, and in many personal-use scenarios it can actually cost more, because the stamp duty for legal entities is 4.25% of the purchase price compared to just 1.5% for individuals.

The main drawback of using a company to own residential property in Sweden is that you lose certain tax benefits available to individual homeowners, you pay nearly three times the stamp duty, and the administrative and accounting costs of maintaining a Swedish AB add ongoing complexity that rarely makes sense for a single home purchase.

Thinking of buying real estate in Sweden?

Acquiring property in a different country is a complex task. Don't fall into common traps – grab our guide and make better decisions.

What taxes and fees will I pay in Sweden in 2026?

What are buyer taxes in Sweden in 2026?

As of early 2026, the main buyer tax when purchasing a house or real property in Sweden is a stamp duty (stampelskatt) of 1.5% of the purchase price for individuals, so on a typical Swedish home priced at SEK 5,000,000 (roughly $560,000 or 473,000 euros), you would pay about SEK 75,000 ($8,400 / 7,100 euros) in stamp duty.

The stamp duty is the only formal buyer tax in Sweden for real property purchases by individuals, and notably there is no stamp duty at all when you buy a cooperative apartment (bostadsratt), which is the most common apartment format in Swedish cities. If you buy through a company instead of as an individual, the stamp duty jumps to 4.25%, which makes it nearly three times more expensive.

Buyer tax rates in Sweden do not differ based on your nationality, so foreign buyers, including Americans, pay exactly the same 1.5% stamp duty as Swedish citizens, and there is no additional surcharge for investment properties versus primary residences.

If you want to go into more details, we also have a page detailing all the property taxes and fees in Sweden.

What are other closing costs in Sweden in 2026?

As of early 2026, total closing costs (excluding stamp duty) for a property purchase in Sweden typically range from about 1% to 3% of the purchase price, so on a SEK 5,000,000 home that means roughly SEK 50,000 to 150,000 ($5,600 to $16,800 / 4,700 to 14,200 euros) depending on whether you need new mortgage deeds.

The main closing cost categories in Sweden include the mortgage deed tax (pantbrev), which is 2% of any new mortgage deed amount plus an admin fee of SEK 375 per deed, the home inspection (besiktning) at around SEK 10,000 to 20,000 ($1,100 to $2,200 / 950 to 1,900 euros) for houses, and for cooperative apartments, a transfer fee of up to about SEK 1,480 and a pledge fee of around SEK 590 based on the 2026 price base amount of SEK 59,200.

In Sweden, the seller typically pays the real estate agent's commission, so that cost is negotiable but not something the buyer directly pays, and the home inspection is optional (though strongly recommended for houses), making it one of the few closing costs a buyer can choose to skip.

The single closing cost that tends to surprise foreign buyers the most in Sweden is the mortgage deed (pantbrev) tax, because at 2% of the new deed amount it can easily add SEK 60,000 to 100,000 ($6,700 to $11,200 / 5,700 to 9,400 euros) on top of everything else, and many buyers from other countries simply do not expect a tax on the mortgage registration itself.

Are there hidden fees foreigners miss in Sweden right now?

Foreign buyers in Sweden commonly overlook between SEK 30,000 and SEK 120,000 ($3,400 to $13,400 / 2,800 to 11,300 euros) in fees they did not initially budget for, depending on the property type and whether new mortgage deeds are needed.

The top three hidden or unexpected fees that foreign buyers in Sweden most often miss are: the 2% mortgage deed tax on new pantbrev registrations, which can easily reach SEK 60,000 to 100,000 ($6,700 to $11,200 / 5,700 to 9,400 euros); the cooperative monthly fee (avgift) for bostadsratt apartments, which can run SEK 3,000 to 8,000 per month and may increase without notice; and the cost of translating and notarizing foreign-language documents, which can add SEK 5,000 to 15,000 ($560 to $1,680 / 470 to 1,420 euros).

The ongoing annual cost that foreign property owners most often underestimate in Sweden is the municipal property fee for houses, which in 2026 is capped at SEK 10,425 ($1,170 / 985 euros) per year or 0.75% of the assessed value (whichever is lower), and for cooperative apartment owners, the monthly avgift that covers the building's maintenance, insurance, and shared debt can rise over time as the cooperative's finances change.

Getting surprised by hidden fees is one of the pitfalls people face when buying real estate in Sweden.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in Sweden versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

Can I get a mortgage as a US citizen in Sweden in 2026?

Do banks lend to US citizens in Sweden in 2026?

As of early 2026, Swedish banks do lend to US citizens, but mortgage approval is more conditional for Americans than for Swedish residents because banks require extra compliance checks and documentation from foreign borrowers.

US citizens generally receive slightly more cautious treatment than other foreign nationals when applying for mortgages in Sweden, not because of Swedish prejudice, but because American borrowers trigger FATCA reporting obligations that add compliance costs and paperwork for the lending bank.

The main reason some Swedish banks are hesitant to lend to American borrowers specifically is FATCA (the Foreign Account Tax Compliance Act), which requires Swedish banks to report US-person accounts to the IRS, creating extra administrative burden that smaller banks especially prefer to avoid.

There is no published approval rate specifically for US citizens, but based on market experience, Americans with stable documented income (Swedish or foreign), a clean financial profile, and at least 15% down payment have a reasonable chance of approval at Sweden's larger banks, while those without Swedish income or residency face a notably harder path.

There is a full document dedicated to mortgage for foreigners in our pack covering the property buying process in Sweden.

What down payment do American people need in Sweden in 2026?

As of early 2026, the minimum down payment for a mortgage in Sweden is effectively 15% of the purchase price, because Sweden's long-standing regulatory cap limits mortgages to 85% loan-to-value, so on a typical SEK 5,000,000 property that means you need at least SEK 750,000 ($84,000 / 70,900 euros) upfront plus closing costs.

While 15% is the regulatory minimum in Sweden, foreign buyers without strong Swedish income documentation or credit history are sometimes asked for 20% to 30% down, so the realistic range for an American buyer in Sweden is 15% to 30% of the purchase price depending on your financial profile.

A larger down payment in Sweden does tend to improve your mortgage terms, because borrowing below 50% or 70% of the property value reduces the mandatory amortisation rate set by Finansinspektionen, which directly lowers your monthly payment and can also help you negotiate a better interest rate with your Swedish bank.

You can also read our latest update about mortgage and interest rates in Sweden.

What interest rates do US citizens get in Sweden in 2026?

As of early 2026, the typical mortgage interest rate in Sweden for a well-qualified borrower is roughly 2.6% to 3.3%, based on the official average for new housing loan agreements of about 2.71% reported by Statistics Sweden (SCB) for November 2025.

Interest rates for foreign buyers in Sweden are generally comparable to those offered to local residents, because Swedish banks price mortgages primarily based on the loan-to-value ratio, the fixation period, and your overall creditworthiness, not on your passport.

Variable-rate mortgages are by far the most common choice in Sweden, even for foreign buyers, because the Swedish market has a long tradition of variable-rate borrowing, and typical fixation periods are either fully variable (3-month) or short-term fixed at 1 to 3 years, with longer fixed terms (5 to 10 years) available but usually at a premium.

The single factor that has the biggest impact on the interest rate a US citizen will be offered in Sweden is your loan-to-value ratio, because borrowing less relative to the property's value significantly reduces the bank's risk and unlocks better pricing, often more so than any other variable in your application.

Can I use US income to qualify in Sweden right now?

Most major Swedish banks will accept US-sourced income for mortgage qualification, but they apply stricter documentation requirements and sometimes a currency discount (haircut) to account for exchange rate risk when your earnings are in dollars rather than Swedish kronor.

Swedish banks typically require American applicants to provide at least two years of US tax returns, recent pay stubs or an employer letter confirming your salary, bank statements showing consistent income deposits, and a full overview of your existing debts including US student loans, credit cards, and any other mortgages.

If standard US income documentation is not enough to satisfy a Swedish bank, some lenders will accept alternative verification such as a CPA-certified income statement, contracts showing future guaranteed income, or proof of substantial liquid assets that demonstrate your ability to service the mortgage even without traditional payroll documentation.

Get fresh and reliable information about the market in Sweden

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

How do US taxes interact with owning property in Sweden?

Do I have to declare the property to the IRS from Sweden?

US citizens who own property in Sweden are not required to file a specific IRS form just for owning a foreign home, but the moment you earn rental income, hold Swedish bank accounts above certain thresholds, or sell the property for a gain, you trigger IRS reporting obligations.

If you earn rental income from your Swedish property, you report it on Schedule E of your US tax return, and if your Swedish financial accounts (used for mortgage payments, rent collection, or deposits) exceed $10,000 at any point in the year, you must file an FBAR (FinCEN Form 114), while Form 8938 may also apply if your foreign financial assets exceed higher thresholds depending on your filing status and residence.

Simply owning a Swedish property without earning income from it or selling it does not, by itself, create a special IRS filing requirement, but the related bank accounts and any income you receive from the property absolutely do, which is why most Americans who buy in Sweden end up with at least some additional US tax paperwork.

Will I pay tax twice in the US and Sweden in 2026?

As of early 2026, the risk of true double taxation for US citizens owning property in Sweden is low in practice, but it is not zero, because the US taxes its citizens on worldwide income regardless of where they live, which means you may owe both Swedish and US tax on the same rental income or capital gain.

The good news is that the United States and Sweden have an active income tax treaty, and this treaty provides mechanisms like foreign tax credits and exemptions to prevent you from paying the full tax rate in both countries on the same income.

The Foreign Tax Credit (Form 1116 on your US return) allows you to offset income taxes paid to Sweden against your US tax bill dollar-for-dollar, so if you pay Swedish tax on rental income, you can generally credit that amount against what you owe the IRS, which in most cases eliminates or greatly reduces any double payment.

Whether Swedish property charges (like the municipal property fee capped at SEK 10,425 in 2026) are deductible on your US federal tax return depends on your specific tax situation and the current US rules around state and local tax deductions, so this is one of those questions where talking to a US CPA who understands cross-border taxation is strongly recommended.

Do I need FATCA reporting when buying in Sweden?

FATCA (the Foreign Account Tax Compliance Act) does not directly apply to the Swedish property itself, but in practice, buying property in Sweden almost always creates FATCA-related reporting obligations because you will open Swedish bank accounts, hold deposits, and possibly set up escrow arrangements that qualify as foreign financial assets.

FATCA reporting via Form 8938 is triggered when your foreign financial assets exceed $50,000 at the end of the year (or $75,000 at any point) for single filers living in the US, with higher thresholds for married couples and US citizens living abroad, so the Swedish bank accounts you open for mortgage payments and property management can easily push you over these limits.

FATCA (Form 8938) and FBAR (FinCEN Form 114) are related but separate obligations: FBAR kicks in when your aggregate foreign account balances exceed $10,000 at any point during the year and is filed with FinCEN, while FATCA Form 8938 has higher thresholds and is filed with your IRS tax return, and many American property owners in Sweden end up needing to file both.

Consulting a US CPA before buying property in Sweden is strongly recommended, and the specific questions worth asking are: how will my Swedish bank accounts affect FBAR and FATCA filing, what foreign tax credits can I claim for Swedish taxes paid, and if I ever sell the property, how will the capital gain be taxed on both the Swedish and US sides.

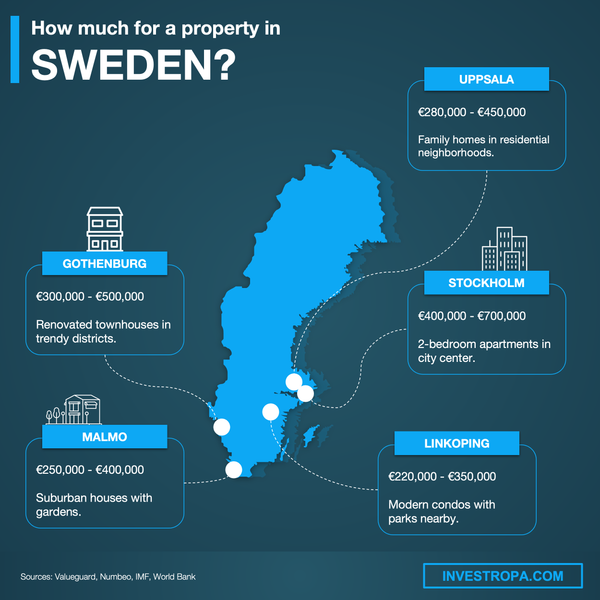

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of Sweden. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Sweden, we always rely on the strongest methodology we can ... and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why we trust it | How we used it |

|---|---|---|

| Lantmateriet | Sweden's official land and property registration authority. | We used it to confirm ownership registration rules, stamp duty rates, and mortgage deed fees. We also relied on it to verify that no citizenship restriction applies to foreign buyers. |

| Skatteverket (2026 amounts) | Sweden's tax authority publishing official annual tax figures. | We used it to pin down the 2026 municipal property fee cap and other tax-related amounts. We also cross-checked it against the property charge guidance page to avoid stale numbers. |

| Skatteverket (non-resident guide) | Official English guidance for non-residents with Swedish tax ties. | We used it to explain how non-resident buyers handle tax registration and reporting. We also relied on it to confirm that buying from abroad is administratively possible. |

| Finansinspektionen (FI) | Sweden's financial regulator setting binding mortgage rules. | We used it to explain the 85% LTV cap and amortisation requirements that shape every buyer's monthly costs. We also used it to ground the mortgage section in regulation rather than bank marketing. |

| Statistics Sweden (SCB) - mortgage rates | Sweden's official statistics agency publishing central bank data. | We used it to anchor our mortgage rate estimates using the latest "new agreements" average. We also used the November 2025 statistical news release to refine our early-2026 rate range. |

| Sveriges Riksbank | Sweden's central bank explaining mortgage rate dynamics. | We used it to explain why Swedish mortgage rates move the way they do. We also used it to ground the interest rate section in Swedish-specific realities like variable-rate dominance. |

| Swedish Government (price base amount) | Official government announcement used in Swedish fee calculations. | We used it to compute 2026 cooperative transfer and pledge fees. We also used it to convert rules-of-thumb into concrete SEK estimates for the current year. |

| SCB (foreign citizens database) | Official population data by citizenship from Statistics Sweden. | We used it to estimate the number of US citizens living in Sweden. We also used it to support the "Americans in Sweden" section with data rather than anecdotes. |

| IRS (Sweden tax treaty) | US tax authority hosting the official treaty texts. | We used it to confirm that a US-Sweden income tax treaty exists and is accessible. We also used it to anchor the "double tax relief" section from the American side. |

| Skatteverket (double taxation) | Sweden's official explanation of how double tax relief works. | We used it to explain the Swedish side of double-tax relief in plain language. We also paired it with the IRS treaty page so our analysis covers both countries. |

Get to know the market before buying a property in Sweden

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.