Authored by the expert who managed and guided the team behind the Sweden Property Pack

Everything you need to know before buying real estate is included in our Sweden Property Pack

Getting a mortgage in Sweden as a foreigner is possible, but the process works differently depending on your residency status and income source.

Swedish banks have strict rules, and the strongest profiles typically belong to people who already live in Sweden and earn Swedish income.

We constantly update this blog post to reflect the latest regulations, tax rates, and market conditions in Sweden.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Sweden.

Can foreigners get a mortgage in Sweden right now?

Can a foreigner get a residential mortgage in Sweden right now?

Yes, foreigners can get a residential mortgage in Sweden, but the process is built primarily for residents who have Swedish banking relationships and documentation.

Foreigners who already live in Sweden, hold a Swedish personal number (personnummer), and earn income locally have the easiest path to mortgage approval in Sweden.

The most common restriction Swedish banks impose on foreign applicants is the requirement to prove stable, verifiable income from Swedish sources, since banks struggle to assess foreign income and enforce repayment abroad.

By the way, we have a whole document dedicated to mortgages for foreigners in our property pack about Sweden.

Can I get a mortgage in Sweden without residency?

Getting a mortgage in Sweden without residency is technically possible, but it is significantly harder because most Swedish banks are set up to serve Nordic residents.

Permanent residents and those with a Swedish personal number (personnummer) qualify most easily, followed by work visa holders with signed Swedish employment contracts, while non-residents face the strictest scrutiny.

For applicants without permanent residency in Sweden, banks typically require larger down payments (often 20% to 40% instead of the standard 15%), stronger income documentation, and sometimes references from banks in the applicant's home country.

By the way, we've written a blog article detailing residency and citizenship options that exist when you buy property in Sweden.

Do banks require a local work contract in Sweden right now?

For most standard Swedish mortgage applications, having a Swedish work contract or Swedish-taxed income is close to a requirement because it makes income verification straightforward for banks.

If you do not have a local work contract, Swedish banks may accept foreign income from stable, long-term employment with well-known international companies, but they typically require extensive documentation including tax returns, bank statements, and employment verification letters.

When a local Swedish work contract is present, banks in Sweden usually want to see at least a few months of employment history, and they pay close attention to whether the employment is permanent or includes a probation period.

Can self-employed foreigners qualify for a mortgage in Sweden?

Yes, self-employed foreigners can qualify for a mortgage in Sweden, but they face extra documentation requirements and banks tend to apply a more conservative approach when calculating their income.

Swedish banks typically require self-employed applicants to provide 2 to 3 years of audited financial statements and tax returns, and they often use the lowest recent income figure rather than an average when assessing affordability.

Is foreign income accepted for mortgages in Sweden right now?

Swedish banks sometimes accept foreign income for mortgage applications, but it is the single factor most likely to complicate or delay your approval because it introduces currency risk and verification challenges.

When your income comes from abroad, Swedish banks typically require comprehensive documentation including 6 to 12 months of bank statements, 2 to 3 years of tax returns, employment verification letters, and sometimes references from your home country bank.

Can I buy a primary home (and an investment property?) with a mortgage in Sweden as a foreigner?

Foreigners can generally obtain a mortgage for a primary home in Sweden, especially if they live in the country and have Swedish income, since banks view owner-occupied properties as lower risk.

Getting a mortgage for an investment property in Sweden as a foreigner is also possible, but banks tend to be more conservative with loan-to-value ratios and may apply stricter affordability criteria for non-primary residences.

If you're buying for investment, you might want to check our blog article about buying and renting out in Sweden.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in Sweden versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What are the eligibility rules banks actually use in Sweden?

What minimum monthly income do I need in Sweden as of 2026?

As of early 2026, there is no official minimum income threshold in Sweden, but banks typically expect a single borrower to earn at least SEK 40,000 to 55,000 per month (roughly USD 3,800 to 5,200 or EUR 3,500 to 4,800) to qualify for a mortgage on an average-priced property.

In practice, most approved borrowers in Sweden fall into the SEK 55,000 to 95,000 monthly income range (USD 5,200 to 9,000 or EUR 4,800 to 8,300), especially for properties in Stockholm, Gothenburg, or Malmö where prices are higher.

The minimum income requirement in Sweden scales directly with the loan amount because banks use affordability models that ensure you can cover mortgage payments, amortization, and living costs even if interest rates rise.

Swedish banks do allow combining household incomes from multiple applicants, so couples or co-borrowers can pool their earnings to meet the income threshold for a larger mortgage in Sweden.

What debt-to-income limit do banks use in Sweden right now?

Swedish banks do not publish a single debt-to-income cap, but the critical threshold in early 2026 is 4.5 times your gross annual income, beyond which stricter amortization rules apply that make the loan more expensive monthly.

When calculating your debt-to-income ratio in Sweden, banks include all existing debts such as car loans, personal loans, student loans, credit card balances, and any other mortgages you may have.

Do I need a local credit score in Sweden right now?

Sweden does not use a credit score system like the United States, but Swedish banks do run credit checks through local credit bureaus (primarily UC) to verify your payment history and look for any negative marks like missed payments.

Foreign credit reports can serve as supporting documentation in Sweden, but they typically do not replace the Swedish credit check, so having a local credit footprint (even a short one) significantly improves your chances of mortgage approval.

Do banks require a local guarantor in Sweden right now?

Swedish banks do not typically require a local guarantor for standard residential mortgages, but they may request one if your profile is considered higher risk (such as being a non-resident, having foreign income, or lacking Swedish credit history).

Banks in Sweden are most likely to request a guarantor when the applicant has a thin credit file, is buying with the maximum loan-to-value ratio, or has income that is difficult to verify through standard Swedish channels.

If a guarantor is required in Sweden, they must typically be a Swedish resident with stable income and a clean credit history, and they become legally responsible for your loan if you default.

Make a profitable investment in Sweden

Better information leads to better decisions. Save time and money. Download our guide.

How much cash do I need upfront in Sweden as of 2026?

What's the minimum down payment in Sweden right now?

The minimum down payment in Sweden in early 2026 is 15% of the property value because Swedish law caps mortgages at 85% loan-to-value, though foreign buyers without strong Swedish ties often need 20% to 40% in practice.

Across different banks and buyer profiles in Sweden, realistic down payment requirements range from 15% for residents with strong Swedish income and credit history to 30% or even 40% for non-residents or those with foreign income.

You may secure a lower down payment requirement in Sweden if you have permanent residency, a Swedish personal number, stable Swedish employment, and an existing relationship with a Swedish bank.

What loan terms can I realistically get in Sweden as of 2026?

What mortgage interest rates are typical in Sweden as of 2026?

As of early 2026, typical mortgage interest rates in Sweden range from about 2.7% to 3.5% for residents with strong profiles, while foreigners (especially non-residents) often pay rates of 3.5% to 4.5% or higher.

The factors that most significantly influence your interest rate in Sweden include your loan-to-value ratio, the strength of your Swedish credit history, whether your income is Swedish or foreign, and how much you negotiate with the bank.

Foreigners in Sweden typically receive interest rates that are 0.1 to 0.9 percentage points higher than Swedish residents because banks view them as higher risk, though this gap narrows significantly for foreigners with strong Swedish ties.

The interest rate is one of the factors we look at when assessing whether now is a good time to buy a property in Sweden.

Are fixed-rate mortgages available in Sweden right now?

Yes, fixed-rate mortgages are available to foreigners in Sweden, and they are a common option alongside variable-rate mortgages that adjust based on market conditions.

Swedish banks typically offer fixed-rate periods of 1, 2, 3, 5, 7, and 10 years, with longer fixed periods providing more payment certainty but usually at a slightly higher initial rate than variable options.

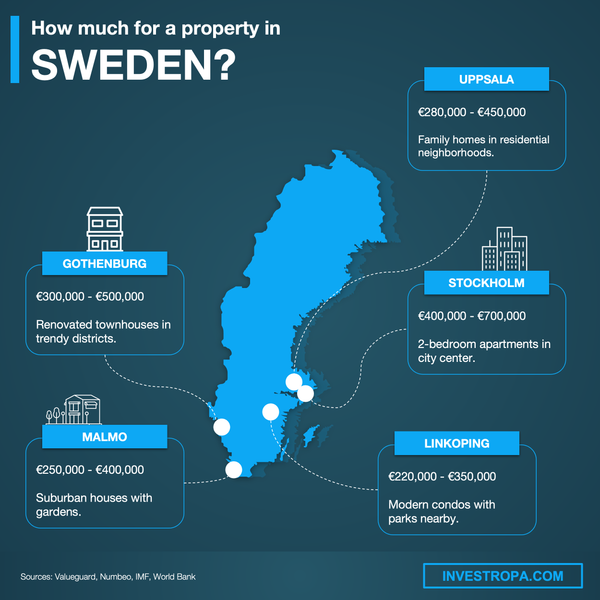

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of Sweden. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

How do I maximize approval chances in Sweden right now?

What financial profile gets "yes" fastest in Sweden right now?

The ideal financial profile for fast mortgage approval in Sweden in early 2026 is a Swedish resident with a personnummer, stable Swedish employment, a clean local credit history, and a down payment larger than the minimum 15%.

Banks in Sweden consider ideal applicants to have monthly income of at least SEK 55,000 to 70,000 (USD 5,200 to 6,600 or EUR 4,800 to 6,100) for single borrowers, with a debt-to-income ratio below 4.5 times gross annual income to avoid stricter amortization requirements.

Swedish banks most favor applicants with permanent employment contracts (not probation or temporary), ideally with at least 6 to 12 months of employment history at their current employer.

A down payment of 30% or more signals a strong applicant profile in Sweden because it keeps your loan-to-value ratio below 70%, which reduces your mandatory amortization requirement and makes you more attractive to lenders.

We give more detailed tips in our pack covering the property buying process in Sweden.

What mistakes make foreigners get rejected in Sweden right now?

The most common mistake that leads to mortgage rejection for foreigners in Sweden is applying at 85% loan-to-value while being a non-resident or having foreign income, because banks internally set much lower LTV limits for higher-risk profiles even though the legal cap allows 85%.

The biggest financial red flag that disqualifies foreign applicants in Sweden is having a debt-to-income ratio above 4.5 times gross income combined with unverifiable foreign income, which triggers stricter amortization rules while also making the bank doubt repayment capacity.

Get to know the market before you buy a property in Sweden

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

Which banks say yes to foreigners in Sweden right now?

Which banks are most foreigner-friendly in Sweden as of 2026?

As of early 2026, the banks considered most foreigner-friendly for mortgages in Sweden include SEB (which has a dedicated "New in Sweden" onboarding process), Swedbank (one of the largest with clear published rates), and SBAB (the state-owned mortgage specialist known for transparent processes).

These banks are more accessible to foreign applicants in Sweden because they have established procedures for handling non-Swedish documentation, dedicated staff who work with international customers, and published guidelines that make requirements clearer.

Which banks accept non-resident borrowers in Sweden right now?

Some banks in Sweden will consider non-resident borrowers on a case-by-case basis, including SEB, Swedbank, and potentially Handelsbanken, but approvals are rare and require strong financial profiles with substantial down payments.

For non-resident applicants in Sweden, these banks typically impose additional requirements including larger down payments (often 30% to 40%), more extensive income documentation, bank references from the applicant's home country, and sometimes proof of connection to Sweden such as family ties or a future relocation plan.

Do international banks lend more easily in Sweden right now?

International banks with Swedish operations (like Handelsbanken, SEB, and Nordea which have Nordic-wide presence) may be more accommodating to foreigners who already have a relationship with them in another country, but Swedish mortgage rules still apply regardless of the bank.

International banks with mortgage offerings in Sweden include Handelsbanken, Nordea, Danske Bank, and SEB, all of which have experience serving international clients across the Nordic region.

The main advantage of using an international bank for a mortgage in Sweden is that existing customers can leverage their relationship history, making income verification and creditworthiness easier to demonstrate across borders.

We made this infographic to show you how property prices in Sweden compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Sweden, we always rely on the strongest methodology we can ... and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source Name | Why It's Authoritative | How We Used It |

|---|---|---|

| Lantmäteriet | Sweden's official land registry and cadastral authority. | We used it to confirm that foreigners follow the same ownership rules as Swedes. We referenced their stamp duty and fee schedules for purchase cost estimates. |

| Finansinspektionen (FI) | Sweden's financial regulator that sets binding mortgage rules. | We used their regulations to document the 85% mortgage cap and amortization requirements. We referenced FFFS 2016:16 for the 4.5x income rule details. |

| Sveriges Riksbank | Sweden's central bank that influences mortgage pricing. | We used their policy rate data to explain why Swedish mortgage rates move. We referenced their economic forecasts for rate trend context. |

| Statistics Sweden (SCB) | Sweden's official statistics agency for economic data. | We used their financial market statistics for official mortgage rate averages. We referenced their dwelling stock data for housing market context. |

| SBAB | State-owned Swedish mortgage specialist with transparent processes. | We used their credit assessment documentation to explain how banks evaluate borrowers. We referenced their lending criteria for foreigner-specific requirements. |

| SEB | Major Swedish bank with dedicated foreigner onboarding. | We used their "New in Sweden" requirements to explain documentation needs. We referenced their policies for non-Swedish citizen mortgage applicants. |

| Swedbank Hypotek | One of Sweden's largest mortgage providers with published rates. | We used their interest rate tables as a primary bank pricing example. We referenced their lending policies for mainstream Swedish mortgage terms. |

| Konsumenternas | Swedish consumer finance bureau explaining how loans work. | We used their credit assessment guides to explain what banks check. We referenced their consumer-focused explanations for plain-language descriptions. |

| Nordea | Major Nordic bank showing residency requirements for services. | We used their "living abroad" policies to illustrate non-resident restrictions. We referenced their Nordic focus to explain why residency matters for bank access. |

| Government of Sweden (Regeringen) | Official source for upcoming Swedish policy changes. | We used their December 2025 proposal to flag potential rule changes after early 2026. We clearly labeled proposed rules as not yet in force. |

Get the full checklist for your due diligence in Sweden

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.