Authored by the expert who managed and guided the team behind the Bulgaria Property Pack

Everything you need to know before buying real estate is included in our Bulgaria Property Pack

Getting a mortgage in Bulgaria as a foreigner is possible, but the process comes with extra steps and stricter requirements compared to what local buyers face.

Bulgarian banks do lend to non-residents and foreign income earners, though they typically ask for larger down payments and more documentation.

We constantly update this blog post to reflect the latest regulations, interest rates, and bank policies in Bulgaria.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Bulgaria.

Fact-checked and reviewed by our local expert

Yeheli Samuels 🇧🇬🇮🇱

CEO and Founder, Dira Bulgarit - Israeli real estate in Bulgaria

Can foreigners get a mortgage in Bulgaria right now?

Can a foreigner get a residential mortgage in Bulgaria right now?

Yes, foreigners can get residential mortgages in Bulgaria in early 2026, though approvals are more selective and cash requirements are typically higher than for Bulgarian residents.

EU citizens and foreigners with permanent or long-term Bulgarian residency generally have the easiest access to mortgages in Bulgaria, since banks can more easily verify their local ties and income stability.

The most common restriction Bulgarian banks impose on foreign applicants is a lower loan-to-value ratio, which means you will need a larger down payment, often 30% or more instead of the 15% minimum that locals might qualify for.

By the way, we have a whole document dedicated to mortgages for foreigners in our property pack about Bulgaria.

Can I get a mortgage in Bulgaria without residency?

Yes, non-residents can obtain mortgages in Bulgaria, though the process is harder and requires stronger financial profiles than resident applicants.

Bulgarian banks generally work with three tiers of borrowers: permanent residents have the easiest path, temporary residents and EU citizens living part-time can often get approved with clean documentation, and non-residents face the strictest requirements but can still succeed with major banks like UniCredit Bulbank.

When you apply without permanent residency in Bulgaria, banks typically require a higher down payment (often 30 to 40%), more extensive income documentation, and may charge slightly higher interest rates to offset their perceived risk.

By the way, we've written a blog article detailing residency and citizenship options that exist when you buy property in Bulgaria.

Do banks require a local work contract in Bulgaria right now?

No, Bulgarian banks do not always require a local work contract, and several major lenders have specific mortgage products designed for borrowers who earn income abroad.

When you lack a local Bulgarian work contract, banks typically accept foreign employment contracts, bank statements showing regular salary deposits, tax returns from your home country, and official income verification documents that have been translated and apostilled.

If you do have a local Bulgarian work contract, banks usually prefer to see at least 6 to 12 months of employment history, though longer tenure makes your application stronger and can help you secure better terms.

Can self-employed foreigners qualify for a mortgage in Bulgaria?

Yes, self-employed foreigners can qualify for mortgages in Bulgaria, though the approval process is typically slower and requires more documentation than for salaried employees.

Bulgarian banks usually require self-employed applicants to show at least 2 years of consistent business history, with stable or growing profits documented through tax returns, financial statements, and business account records.

Is foreign income accepted for mortgages in Bulgaria right now?

Yes, several major Bulgarian banks explicitly accept foreign income for mortgage applications, with Fibank and Postbank both marketing specific products for borrowers earning money outside Bulgaria.

When your income comes from abroad, Bulgarian banks typically require translated and apostilled employment contracts, 6 to 12 months of bank statements showing salary deposits, tax documents from your home country, and often proof that your income originates from lower-risk jurisdictions like the EU, UK, US, or Canada.

Can I buy a primary home (and an investment property?) with a mortgage in Bulgaria as a foreigner?

Yes, foreigners can obtain mortgages for primary homes in Bulgaria, and this is actually the most bank-friendly use case since lenders view owner-occupiers as lower risk borrowers.

Investment property mortgages are also possible for foreigners in Bulgaria, but banks typically apply stricter underwriting with higher down payment requirements and may discount or ignore projected rental income unless you can prove existing lease agreements.

If you're buying for investment, you might want to check our blog article about buying and renting out in Bulgaria.

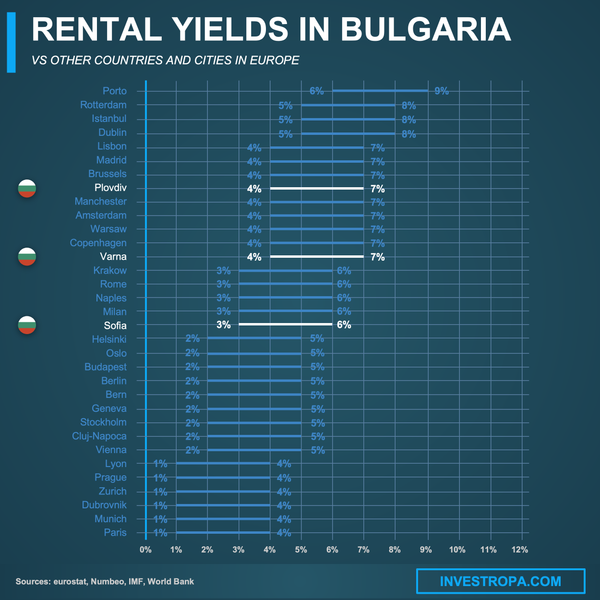

We did some research and made this infographic to help you quickly compare rental yields of the major cities in Bulgaria versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What are the eligibility rules banks actually use in Bulgaria?

What minimum monthly income do I need in Bulgaria as of 2026?

As of early 2026, there is no single published minimum income for Bulgarian mortgages, but banks effectively back into it from the 50% debt-service-to-income cap, meaning your monthly payment cannot exceed half your verified net income.

In practice, most approved foreign borrowers in Bulgaria have net monthly incomes of at least 3,000 to 5,000 BGN (roughly 1,500 to 2,500 EUR or 1,600 to 2,700 USD), which provides comfortable room within the DSTI limits for typical loan amounts.

The minimum income you need in Bulgaria scales directly with the property price and loan amount: a 200,000 BGN loan with a 1,200 BGN monthly payment needs at least 2,400 BGN net income at the 50% cap, but banks prefer seeing 3,000 BGN or more for smoother approval.

Bulgarian banks do allow combining household incomes from co-applicants to meet the threshold, which can help couples or family members qualify for larger loans together.

What debt-to-income limit do banks use in Bulgaria right now?

Bulgarian banks must cap your total debt service at 50% of your monthly disposable income (after taxes and mandatory contributions), as mandated by the Bulgarian National Bank's borrower-based measures that took effect in 2024.

When calculating this ratio, Bulgarian banks include all your existing debt payments: credit card minimum payments, car loans, personal loans, student loans, and any other mortgages you already hold, not just the new mortgage payment you are applying for.

Do I need a local credit score in Bulgaria right now?

No, Bulgarian banks do not strictly require a local credit score for mortgage approval, especially if your income is strong, your down payment is substantial, and your documentation is clean and complete.

Bulgarian banks can accept foreign credit reports as supporting evidence of your creditworthiness, but they rely more heavily on reviewing your bank statements, verifying your income directly, and assessing the quality of the property you want to buy.

Do banks require a local guarantor in Bulgaria right now?

No, Bulgarian banks do not usually require a local guarantor for foreign mortgage applicants, though this can come up in specific edge cases where your profile has weaknesses.

Banks in Bulgaria are most likely to request a guarantor when your credit file is thin, your debt-to-income ratio is borderline close to 50%, your foreign income is complex to verify, or the property has unusual legal characteristics.

If a Bulgarian bank does ask for a guarantor, that person typically needs to be a Bulgarian resident with stable income and a clean credit history, capable of covering the loan payments if you default.

Make a profitable investment in Bulgaria

Better information leads to better decisions. Save time and money. Download our guide.

How much cash do I need upfront in Bulgaria as of 2026?

What's the minimum down payment in Bulgaria right now?

The regulatory minimum down payment in Bulgaria is 15% (based on the BNB's 85% loan-to-value cap), but foreign buyers should realistically plan for 30 to 40% down to get smooth approvals from Bulgarian banks.

Across different Bulgarian banks and buyer profiles, down payment requirements typically range from 15% for residents with excellent profiles to 30 to 40% for non-residents and foreign income earners, with Fibank explicitly showing 30% down (70% financing) for its foreign income product.

You might secure a lower down payment closer to 20 to 25% in Bulgaria if you have permanent residency, strong local banking history, stable employment with a Bulgarian company, or an exceptionally high income that keeps your DSTI ratio well below 40%.

What loan terms can I realistically get in Bulgaria as of 2026?

What mortgage interest rates are typical in Bulgaria as of 2026?

As of early 2026, typical mortgage interest rates for foreigners in Bulgaria range from about 2.5% to 5.5% variable, with residents getting rates around 2.4 to 3.2% while non-residents and foreign income earners often see rates between 3.8% and 5.5%.

The factors that most significantly influence your Bulgarian mortgage interest rate include your down payment size, your residency status, whether your income is local or foreign, and the overall strength of your documentation and financial profile.

Yes, foreigners typically receive higher interest rates than Bulgarian residents, often paying 1 to 2 percentage points more: for example, while the BNB reported an average rate of 2.47% for residents in September 2025, Fibank's foreign income product shows 4.11%.

The interest rate is one of the factors we look at when assessing whether now is a good time to buy a property in Bulgaria.

Are fixed-rate mortgages available in Bulgaria right now?

True long-term fixed-rate mortgages (like 20 or 30-year fixed rates common in some countries) are not the standard product in Bulgaria, where most mortgages use variable rates priced as a bank reference rate plus a margin.

Some Bulgarian banks offer fixed or discounted introductory periods for the first 1 to 5 years, but the core loan structure typically converts to variable after that period, so borrowers should plan for rate changes over the life of their loan.

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of Bulgaria. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

How do I maximize approval chances in Bulgaria right now?

What financial profile gets "yes" fastest in Bulgaria right now?

The ideal financial profile for fast mortgage approval in Bulgaria combines a high down payment (30% or more), a low debt-to-income ratio (under 35 to 40%), stable salaried employment, clean bank statements, and a property with clear legal title in a liquid market.

Bulgarian banks consider an ideal fast-approval profile to have net monthly income of at least 4,000 to 6,000 BGN (roughly 2,000 to 3,000 EUR or 2,200 to 3,200 USD) with a debt-to-income ratio comfortably below 35%, even though the legal cap allows up to 50%.

Banks in Bulgaria most favor applicants with stable salaried employment and at least 1 to 2 years of tenure with the same employer, as this demonstrates income reliability and makes verification straightforward.

A down payment of 30 to 40% signals a strong applicant profile in Bulgaria, as it significantly reduces the bank's risk and often leads to better interest rates and faster processing.

We give more detailed tips in our pack covering the property buying process in Bulgaria.

What mistakes make foreigners get rejected in Bulgaria right now?

The most common mistake that leads to mortgage rejection for foreigners in Bulgaria is buying a property with complicated legal status, such as unclear land ownership rights, missing cadastre documents, or encumbrances that the buyer did not check through the Property Register before making an offer.

The financial red flag that most often disqualifies foreign applicants in Bulgaria is trying to count projected rental income to qualify for the loan, since Bulgarian banks typically discount or completely ignore rental income unless you can prove existing lease agreements with documented payment history.

Get to know the market before you buy a property in Bulgaria

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

Which banks say yes to foreigners in Bulgaria right now?

Which banks are most foreigner-friendly in Bulgaria as of 2026?

As of early 2026, the most foreigner-friendly banks for mortgages in Bulgaria include UniCredit Bulbank (which explicitly offers a "Mortgage Loan without Permanent Residence"), Fibank (with specific foreign income products), Postbank (targeting Bulgarians working abroad), UBB, and DSK Bank.

What makes these Bulgarian banks more accessible to foreign applicants is that they have standardized products and underwriting processes specifically designed for non-residents and foreign income earners, rather than treating each foreign application as an exception requiring special approval.

Which banks accept non-resident borrowers in Bulgaria right now?

UniCredit Bulbank explicitly accepts non-resident borrowers in Bulgaria with their dedicated "Mortgage Loan without Permanent Residence" product, and other major banks like Fibank, UBB, and DSK may also consider non-resident applications on a case-by-case basis.

For non-resident applicants, these Bulgarian banks typically impose higher down payment requirements (often 30 to 40%), request more extensive income documentation with translations and apostilles, and may charge interest rates 1 to 2 percentage points higher than resident borrowers receive.

Do international banks lend more easily in Bulgaria right now?

Yes, international bank groups operating in Bulgaria often lend more easily to foreigners because they have more standardized compliance processes for handling cross-border documents and foreign income verification.

Major international banking groups with Bulgarian operations offering mortgages to foreigners include UniCredit (UniCredit Bulbank), OTP Group (DSK Bank), KBC Group (UBB), and Eurobank (Postbank).

The main advantage of using an international bank for a mortgage in Bulgaria is their experience processing foreign documentation, which can mean smoother handling of translated contracts, foreign credit reports, and income verification from other countries.

We made this infographic to show you how property prices in Bulgaria compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Bulgaria, we always rely on the strongest methodology we can and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why it's authoritative | How we used it |

|---|---|---|

| Bulgarian National Bank (BNB) | It's the central bank that sets binding lending limits for all Bulgarian banks. | We used it to anchor the LTV, DSTI, and maturity caps that shape every mortgage offer. We translated those caps into practical rules for foreign buyers. |

| European Systemic Risk Board (ESRB) | It's the EU body that publishes official notifications of national lending restrictions. | We used it to verify the exact definitions of LTV and DSTI calculations. We also confirmed the start dates and exception allowances. |

| BNB Interest Rate Statistics | It's official central bank reporting of actual bank pricing, not marketing rates. | We used it to establish typical mortgage pricing before early 2026. We adjusted these averages for foreign-income products based on bank-specific data. |

| UniCredit Bulbank | It's a major Bulgarian bank explicitly advertising mortgages for non-residents. | We used it to confirm that non-resident mortgages exist in mainstream Bulgarian banking. We shaped our "which banks say yes" analysis around this evidence. |

| Fibank | It's a bank page with concrete foreign-income lending terms including rates and LTV. | We used it as a hard number anchor for foreign-income mortgage costs. We referenced its 4.11% rate and 70% maximum financing as real-world benchmarks. |

| Postbank | It's a major bank showing specific products for people working abroad. | We used it to demonstrate that "income abroad" is a standard bank category in Bulgaria. We referenced its requirements to explain what banks expect from such borrowers. |

| UBB (United Bulgarian Bank) | It's a major bank showing the real document stack and rate methodology. | We used it to build a realistic step-by-step process and document checklist. We also explained how Bulgarian mortgages price off reference rates plus margins. |

| National Statistical Institute (NSI) | It's the official wage benchmark that helps translate DSTI limits into income thresholds. | We used it to anchor income examples showing typical Bulgarian salaries. We built DSTI-based affordability scenarios from this official baseline. |

| Registry Agency (EPZEU) | It's the official gateway to Bulgaria's Property Register services. | We used it to describe how ownership and encumbrances are verified. We explained what banks' lawyers check during the mortgage process. |

| Constitution of Bulgaria | It's the official publication of Bulgaria's constitutional text including property rights. | We used it to ground the "foreigners can or can't own what" discussion. We turned constitutional rules into a practical checklist for foreign buyers. |

Get the full checklist for your due diligence in Bulgaria

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.